Managing the tax implications of transactions with IP rights

28 September 2023

Taxation is essential for funding public spending and fostering a nation’s economic development. As such, intellectual property rights have also gained popularity in recent years as a priceless resource that may considerably boost a nation’s economy. This has resulted to taxation laws now covering IP rights. IP is transferred either through assignment or licensing, both of which have different tax ramifications. A strong tax structure for IP rights would demonstrate how well an IP regime would function in a country.

“Taxation has a significant impact on the development and commercialization of IP rights due to the way tax treatment and incentives are applied,” said Sudhir Ravindran, attorney-at-law, solicitor and founder of Altacit Global in Chennai. “In the past, the relationship between IP rights and taxation was not prominent. However, as IP rights gained prominence in commercial transactions, the tax system had to adapt to keep up with the changes. The primary purpose of taxation is to generate revenue for government expenditures, and as economic activities involving IP rights increased, the connection between taxation and IP rights became more robust. Today, transactions involving IP rights are subject to various forms of taxation.”

IP rights laws do not generally contain provisions relating to taxation laws since they are of differential characters. Taxation laws, however, rely on the provisions of IP rights law to determine the nature of transaction and monetary considerations, such as royalty payments, rights holder and assignability, among others, to determine the applicability of taxation.

In Singapore, the tax treatments of IP rights and their related transactions are set out in the Income Tax Act and/or the Economic Expansion Incentives (Relief from Income Tax) Act, and not the respective laws governing the various IP rights (Copyrights Act, Patents Act). That said, IP law considerations may come into play when determining the tax treatment of IP rights-related transactions in a restructuring exercise. As an example, where a licence for IP rights is granted to a company, one consideration is whether the company can take the position that it has acquired economic ownership of the IP rights, such that it can claim writing-down allowances on the IP rights in Singapore.

IP rights under taxation regimes

According to Ravindran, IP rights are subject to various accounting treatments under different taxation regimes. How they are classified – either as capital or revenue expenditure under income tax laws – determines whether they are treated as assets or revenue expenses. When transactions involving IP rights occur, such as selling or licensing them, he said they become trigger points for taxation and the income generated from these transactions is taxable under the relevant tax laws.

“Transborder transactions involving IP rights, which occur across national borders, are also subject to taxation in specific countries. However, taxing such transactions can be challenging due to the intangible nature of IP rights, which doesn’t involve physical movement like traditional goods,” he further said. “In certain jurisdictions, instruments that document IP rights transactions are also subject to taxation, meaning that legal agreements, licenses, or contracts related to IP rights may attract taxes based on the applicable laws.”

For Jaclyn Ho, principal and tax advisor at Baker McKenzie Wong & Leow in Singapore, IP rights are not taxed per se. However, she said that what countries are competing for is the tax on the income derived by companies on the commercialization and exploitation of IP rights, and for some, the gain on disposal of the IP rights.

“In fact, IP rights and its corresponding activities, such as R&D, came into the spotlight in 2015 when BEPS Action 5 on Countering Harmful Tax Practices was introduced by the OECD to combat regimes that facilitate base erosion and profit shifting,” she said. “Given the intangible nature of IP rights, the provision of IP rights was regarded as a geographical mobile activity that could be used to shift profits across jurisdictions which offer various preferential tax treatments. To level the playing field, the ‘nexus approach’ was introduced as a substantial activity requirement for IP regimes. This means that the extent to which companies may benefit from an IP regime, such as a concessionary tax rate incentive, in a jurisdiction is linked to the amount of qualifying R&D expenses incurred that gave rise to the IP income.”

When it comes to ownership and management of IP rights, jurisdictions may provide for tax amortization on the IP rights acquired, as this helps reduce a company’s taxable income in that jurisdiction. For example, in Singapore, writing-down allowances can be claimed on capital expenditure incurred in the acquisition of certain IP rights (which includes patents, copyrights and trademarks), subject to conditions.

“Where a company decides to in-license the IP rights which may comprise patents, copyrights and trademarks instead, such royalty payments made to a non-resident would usually attract withholding tax,” she said. “Certain jurisdictions may provide a reduction in the withholding tax rate to encourage companies to access technology and know-how for their activities in-country. In Singapore, there is the Approved Royalties Incentive that provides a tax exemption or a concessionary withholding tax rate on approved royalties, subject to conditions.”

Turning to the commercialization of IP rights, whether and how the income will be taxed would depend on the characterization of the income, and the source rules that follow. “Many jurisdictions provide for a preferential tax rate on the income derived from the commercialization of the rights,” she said. “Depending on the characterization of the income derived from the rights, different regimes may be applicable. In Singapore, the IP Development Incentive provides a concessionary tax rate on qualifying IP income derived by a company as consideration for the commercial exploitation of patents and copyrights subsisting in software. The IP Development Incentive adopts the modified nexus approach set by the OECD in BEPS Action 5.”

IP rights are now a major force behind innovation and economic prosperity. However, they also bring up intricate tax ramifications for people, companies and governments. To maintain compliance and maximize the advantages of these priceless intangible assets, stakeholders must be knowledgeable about the tax laws and regulations relevant to intellectual property.

To successfully navigate the complex web of intellectual property tax rules and regulations, tax experts’ counsel can be helpful. Understanding the tax consequences of intellectual property rights will continue to be a crucial component of successful company strategies as the global economy continues to rely on knowledge-based assets.

Royalties and tax

Carina Laforteza, a partner at SyCip Salazar Hernandez & Gatmaitan in Manila, said the income derived from licensing the use of IP rights – for example, royalties – is subject to tax. She explained royalties are considered as active income subject to regular income tax if a taxpayer generates royalties in the active pursuit and conduct of its primary business purpose. On the other hand, if the royalties are merely incidental to the taxpayer’s primary business purpose, royalties are considered passive income subject to a final withholding tax.

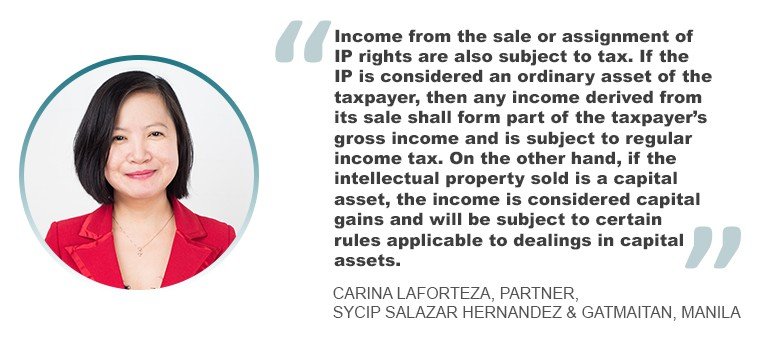

“Income from the sale or assignment of IP rights are also subject to tax. If the IP is considered an ordinary asset of the taxpayer, then any income derived from its sale shall form part of the taxpayer’s gross income and is subject to regular income tax,” she said. “On the other hand, if the intellectual property sold is a capital asset, the income is considered capital gains and will be subject to certain rules applicable to dealings in capital assets.”

Value-added tax is also due on royalties and ordinary gains from the sale of IP rights.

Laforteza said: “The tax code provides that ‘goods’ or ‘properties’ subject to VAT are understood to include intangible objects capable of pecuniary estimation, such as the right or privilege to use patent, copyright, design or model, plan, secret formula or process, goodwill, trademark, trade brand or other like property or right. In the Philippines, Section 88.4 of the IP code provides that Philippine taxes on all payments relating to technology transfer arrangements, which includes the licensing of all forms if IP rights, must be borne by the licensor.”

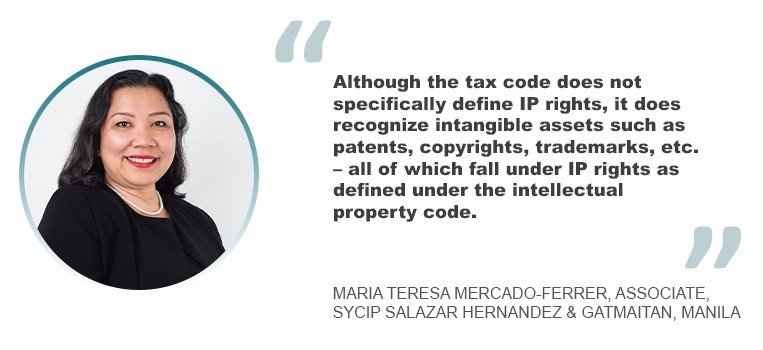

“However, it is possible to ask for an exemption from this provision with respect to value-added tax, which is an indirect tax and generally shifted to the licensee,” added Maria Teresa Mercado-Ferrer, an associate at SyCip Salazar Hernandez & Gatmaitan. “Although the tax code does not specifically define IP rights, it does recognize intangible assets such as patents, copyrights, trademarks, etc. – all of which fall under IP rights as defined under the intellectual property code.”

Being intangible assets, Section 42 of the country’s tax code provides for the situs of income derived from IP rights and states that rentals and royalties from the following are considered as income from sources within the Philippines:

- Use or the privilege to use in the Philippines any copyright, patent, design or model, plan, secret formula or process, goodwill, trademark, trade brand or other like property or right;

- The use of or the right to use in the Philippines any industrial, commercial or scientific equipment;

- The supply of scientific, technical, industrial or commercial knowledge or information;

- The supply of any assistance that is ancillary and subsidiary to and is furnished as a means of enabling the application or enjoyment of any such property or right as mentioned in paragraph (a), any such equipment as mentioned in paragraph (b) or any such knowledge or information as mentioned in paragraph (c);

- The supply of services by a nonresident person or his employee in connection with the use of property or rights belonging to or the installation or operation of any brand, machinery or other apparatus purchased from such nonresident person;

- Technical advice, assistance or services rendered in connection with technical management or administration of any scientific, industrial or commercial undertaking, venture, project or scheme; and

- The use of or the right to use – motion picture films; films or video tapes for use in connection with television; and tapes for use in connection with radio broadcasting.

- Excel V. Dyquiangco